Former market downturn vanished from the Lithuanian housing market

The year 2017 in the Lithuanian housing market was one of the most productive and active in the history of Lithuania. The aggregate Lithuanian housing market activity and financial indicators exceeded the results achieved in 2016 and were only lower than the 2007 indicators. At the same time a faster growing contribution of the regions (other than Vilnius region) into the Lithuanian housing market was also recorded.

According to the State Enterprise Centre of Registers, in 2017 nearly EUR 1.88 billion or 7% more than in 2016 was spent for the acquisition of residential property (apartments and houses). However, trends differ between major cities. In Vilnius, nearly EUR 889 million was spent on the acquisition of housing in 2017 or 1% less than in 2016. In the meantime, in Kaunas the largest positive change was recorded among all major cities – with nearly EUR 235 million spent on the acquisition of housing or a massive 24% more than in 2016. An increase of 7% on housing expenditure was recorded in Klaipėda (nearly EUR 157 million), in Šiauliai – 6% (almost EUR 55 million) and in Panevėžys – 21% more than in 2016 (over EUR 37 million).

According to the State Enterprise Centre of Registers, in 2017 nearly EUR 1.88 billion or 7% more than in 2016 was spent for the acquisition of residential property (apartments and houses). However, trends differ between major cities. In Vilnius, nearly EUR 889 million was spent on the acquisition of housing in 2017 or 1% less than in 2016. In the meantime, in Kaunas the largest positive change was recorded among all major cities – with nearly EUR 235 million spent on the acquisition of housing or a massive 24% more than in 2016. An increase of 7% on housing expenditure was recorded in Klaipėda (nearly EUR 157 million), in Šiauliai – 6% (almost EUR 55 million) and in Panevėžys – 21% more than in 2016 (over EUR 37 million).

Similar trends can be observed in the investment per capita for the acquisition of residential property in the major cities of the country. In 2017, the residents of Vilnius spent the largest amount on the purchase of apartments and houses – EUR 1,626 per capita on average or 1% less than in 2016. The second highest level of housing expenditure per capita was recorded in Klaipėda – EUR 1,049 or 9% more than in 2016. Although Kaunas comes third according to per capita expenditure for the purchase of housing in 2017, the largest positive change was recorded here among the major cities – an average of EUR 809 per capita or a massive 27% increase compared to 2016. The average figure in Šiauliai was EUR 546 (8% more than in 2016) and in Panevėžys – EUR 415 (25% more than in 2016).

Despite a slight increase in mortgage rates in Lithuania, the overall favourable situation in the loan market further stimulated the Lithuanian housing market in 2017. According to the Bank of Lithuania, the average interest rate on new housing loans in 2017 was 2.01% (in 2016 – 1.95% and in 2015 – 1.88%). At the same time the mortgage lending volume and the total housing loan portfolio in Lithuania reached new heights. According to the Bank of Lithuania, in 2017 the remaining loan balance in Lithuania increased by 9.1% to EUR 7.0 billion reaching a historical peak. In 2017, new loans in the amount of EUR 1,178 million were issued in Lithuania and this is almost 12% more than in 2016.

According to the State Enterprise Centre of Registers, the same number of purchase and sale transactions for apartments were concluded in Lithuania in 2017 as in 2016 (33,179 in 2016 and 33,176 in 2017), and 7% more purchase and sale transactions for houses than in 2016 (9,845 in 2016 and 10,529 in 2017). Looking from the historic perspective, the year 2017 was one of the most active in Lithuania and only in 2005 and 2007 the number of residential property transactions was higher. However, trends differ between major cities. In Vilnius, Šiauliai and Klaipėda a decrease in the number of housing transactions (apartments and houses) was recorded compared to 2016: by 6% in Vilnius and Šiauliai and by 2% in Klaipėda. In the meantime, an increase of 5% was recorded in Panevėžys and 4% – in Kaunas. In terms of the relative scope of the transactions per 1,000 citizens, Klaipėda took over the lead from Vilnius in 2017 with the sale of 21.6 apartments/houses per 1,000 citizens, 20.3 – in Vilnius, 18.3 – in Kaunas, 18.0 – in Šiauliai, and 15.3 – in Panevėžys.

Positive economic development in the country encouraged further increase in the prices of the residential property in 2017, yet the relative changes in major cities were somewhat more modest than in 2016. Of all major cities, a faster increase than in 2016 was only recorded in Kaunas. According to data from Ober-Haus, apartment prices in Kaunas increased by an average of 4.8% in 2017 – the price for relatively old apartments increased by an average of 3.0% and for newly constructed apartments – by 8.8%. In Vilnius, Panevėžys, Šiauliai and Klaipėda an increase in the prices of apartments of 3.6%, 3.1%, 2.7% and 2.4% respectively was recorded. The fastest (4% on average) annual growth in the prices of private houses in 2017 was recorded in Vilnius and its suburbs. An increase by an average of 3% in the sale prices of houses was recorded in the regions of Klaipėda, Šiauliai and Panevėžys and an increase by an average of 1% was recorded in Kaunas and its suburbs.

Despite the rapid increase in the supply of apartments for renting in Vilnius over the past years and therefore forecasts regarding a decrease in rents, a symbolic 1% increase in rents was recorded in Vilnius in 2017. The rental market of the capital city remains active and the new supply was substantially absorbed at the same rent levels as in 2016. In the meantime, lower availability of apartments for renting in Kaunas and Klaipėda (especially newly constructed apartments) caused a slightly faster increase in rents in 2017. Rents in Kaunas increased by an average of 4% and in Klaipėda – by 7%. In 2017, the average rent of a 1-3 room apartment in Vilnius was 384 EUR/month, in Kaunas – 295 EUR/month, in Klaipėda – 291 EUR/month, in Šiauliai – 163 EUR/month and in Panevėžys – 137 EUR/month.

The year 2017 saw further growth in investment in construction of new residential buildings in Lithuania. According to Statistics Lithuania, construction works (new construction, reconstruction, repair, restoration, etc.) totalling almost EUR 456 million were performed in the residential property market in 2017 (almost 18% of all construction works performed in the country) or 4.5% less than in 2016 (prices of 2016). However, almost 7% growth in the volume of new construction works was recorded in Lithuania last year.

Experienced developers and higher-class apartment projects prevail

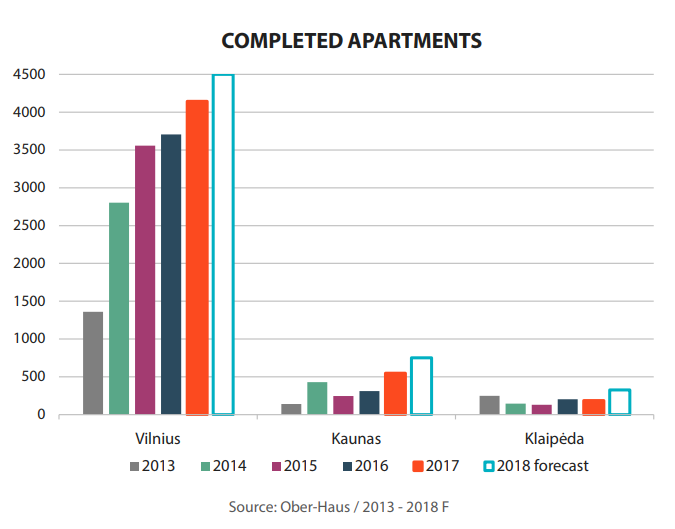

According to data from Ober-Haus, 4,144 apartments in apartment buildings were built in Vilnius in 2017 or 12% more than in 2016. A total of 48 different projects of apartment buildings or their stages were completed in the capital city in 2017. The number of new apartments was the largest since 2008 when 5,471 apartments were built in Vilnius. Projects completed in 2017 were very diverse (in terms of quantity, geography and quality), yet developers tended to invest in the construction of higher class and more expensive apartments. The share of such apartments (the price of the apartments without final fit-out is in excess of 2,000 EUR/sqm) increased from 13% to 18% in the overall annual supply in 2017. These are the projects which offer apartments in the most expensive areas of the city of Vilnius – the centre, the Old Town and other prestigious areas. The share of the medium class apartments (the price of the apartments without final fit-out is between 1,500 EUR/sqm and 1,900 EUR/sqm) in 2017 increased from 48% to 52%. In the meantime, the share of economy class apartments (the price of the apartments without final fit-out is up to 1,500 EUR/m2) decreased from 39% to 30%.

In 2017, experienced developers dominated in the new apartment construction market in Vilnius and the portion of the companies not known in the market (newcomers) decreased compared to 2016. In response to the favourable situation in the market, experienced developers increased their investment portfolio in the residential property market focusing on large-scale projects, while the newcomers developed small projects. Experienced developers, each of which has completed at least four different residential projects, constructed 66% of all apartments in the capital city (in 2016, this figure was 58%). Less experienced developers, each of which has completed 2–3 projects, constructed 24% of all apartments (the figure for 2016 was 21%). The share of apartments constructed by new companies, which do not have any housing development history (i.e. have implemented not more than one project or are only beginning their operations), decreased in 2017 from 21% to 10%. The year 2018 in the apartment market in Vilnius looks promising – construction of at least 4,500 new apartments is scheduled.

More active development of detached and semi-detached houses, which started in 2015–2016, is bearing fruit. In 2017, developers built around 490 new houses in Vilnius and its suburbs or 54% more than in 2016 and twice as many as in 2015. At the same time it is the highest annual supply indicator over the past 15 years (only in 2007, a similar number of houses was supplied to the market). Construction of even a larger number of detached and semi-detached houses is planned in Vilnius and its suburbs in 2018, which could reach up to 550 units. Sales of new houses inspire optimism of developers – at the end of 2017, 85% of the completed houses were sold and reserved.

A rapid increase in supply of newly constructed apartments was recorded in Kaunas in 2017. According to data from Ober-Haus, a total of 547 apartments were built in Kaunas in 2017, which is a 76% increase compared to 2015. The year 2018 promises to be even more productive – construction of 700-800 new apartments in apartment buildings in Kaunas is planned. Six apartment building projects or project stages were implemented in Klaipėda in 2017, which offered 186 apartments (8% less compared to 2016). In the period between 2010 and 2017, on average 200 new apartments in apartment buildings were constructed in Klaipėda each year, but developers did not engage in any further active development projects. However, in 2018 more active development is planned, as a result of which 300–350 new apartments should be offered to the market.

A rapid increase in supply of newly constructed apartments was recorded in Kaunas in 2017. According to data from Ober-Haus, a total of 547 apartments were built in Kaunas in 2017, which is a 76% increase compared to 2015. The year 2018 promises to be even more productive – construction of 700-800 new apartments in apartment buildings in Kaunas is planned. Six apartment building projects or project stages were implemented in Klaipėda in 2017, which offered 186 apartments (8% less compared to 2016). In the period between 2010 and 2017, on average 200 new apartments in apartment buildings were constructed in Klaipėda each year, but developers did not engage in any further active development projects. However, in 2018 more active development is planned, as a result of which 300–350 new apartments should be offered to the market.

Last year the number of unsold new apartments increased in Vilnius only

The overall decrease in the activity of the new apartment market in major cities in 2017 was due to lower sales volumes in the country’s capital. On the contrary, sales volumes in other cities of the country increased. According to data from Ober-Haus, a total of 4,957 new apartments were purchased or reserved directly from the builders in completed apartment buildings and apartment buildings in progress in Vilnius, Kaunas and Klaipėda in 2017. This was a decrease of almost 7% compared to 2016. In 2017, 3,851 new apartments were sold/reserved in Vilnius, a 12% decrease compared to 2016. This should not come as a surprise, because the sales indicators for new apartments achieved in Vilnius in 2016 were the highest in the past eight years and would be hard to replicate. In 2017, 723 new apartments (a 25% increase compared to 2016) were realised in Kaunas and 383 apartments (a 1% increase compared to 2016) in Klaipėda.

Large scale construction of new apartments in the country’s capital in 2017 determined an increase in the number of vacant apartments in completed apartment buildings while, on the contrary, the figures for Kaunas and Klaipėda decreased. By the end of 2017, the total number of unsold apartments in completed apartment buildings in the three cities was 1,888, which was an increase of 9% compared to 2016. By the end of 2017, 1,359 apartments were offered for sale in apartment buildings in Vilnius built in 2007–2017 (there were 1,013 vacant apartments by the end of 2016); this figure was 151 for Kaunas (239 vacant apartments by the end of 2016) and 378 for Klaipėda (485 vacant apartments by the end of 2016). Until there is any slowdown in the construction of new apartments in the country’s capital, the number of unsold apartments will remain stable or will increase slightly. The largest number of unsold apartments in newly completed apartment buildings was recorded at the end of 2015 and totalled over 1,400. High sales volumes reduced the figure to nearly 900 vacant apartments at the beginning of 2017. The situation in Kaunas and Klaipėda is the opposite – increasing demand for new housing and moderate construction volumes decreased the number of vacant apartments in the course of 2017.

People’s financial capacity for buying housing continues to grow

The ratio between the price of apartments and the level of wages in major cities of the country in 2017 continued to improve for the benefit of buyers. According to Statistics Lithuania, the average net wages in Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys in 2017 increased by 5.6–9.6% on average as compared to 2016. According to data from Ober-Haus, the average price of apartments in these cities over the same period increased by 2.7–5.2% (average prices of 2017 compared to average prices of 2016). So statistically residents of these cities were able to buy more residential property in 2017.

According to data from Ober-Haus, a resident of Vilnius was able to purchase 6.2 sqm in a medium class apartment for the average net annual wage (5.9 sqm in 2016); a resident of Kaunas – 7.9 sqm (7.6 sqm in 2016), a resident of Klaipėda – 8.0 sqm (7.8 sqm in 2016), a resident of Šiauliai – 11.7 sqm (11.3 sqm in 2016) and a resident of Panevėžys – 13.3 sqm (12.7 sqm in 2016).

,Despite the improving statistical ratio between the price of apartments and the level of wages, each case of home purchase may be different. For example, some buyers due to their growing personal needs opt for a more expensive home instead of an affordable home which would be easier to pay for. It is only natural that when borrowing for a more expensive home, the financial burden will be higher, therefore these buyers may not often feel the improving statistical ratio between the price of apartments and the level of wages,’ Mr Reginis said.

Lithuania Residential Market Commentary Q4 2017

The year 2017 in the Lithuanian housing market was one of the most productive and active in the history of Lithuania. The aggregate Lithuanian housing market activity and financial indicators exceeded the results achieved in 2016 and were only lower than the 2007 indicators. At the same time a faster growing contribution of the regions (other than Vilnius region) into the Lithuanian housing market was also recorded.

According to the State Enterprise Centre of Registers, in 2017 nearly EUR 1.88 billion or 7% more than in 2016 was spent for the acquisition of residential property (apartments and houses). However, trends differ between major cities. In Vilnius, nearly EUR 889 million was spent on the acquisition of housing in 2017 or 1% less than in 2016. In the meantime, in Kaunas the largest positive change was recorded among all major cities – with nearly EUR 235 million spent on the acquisition of housing or a massive 24% more than in 2016. An increase of 7% on housing expenditure was recorded in Klaipėda (nearly EUR 157 million), in Šiauliai – 6% (almost EUR 55 million) and in Panevėžys – 21% more than in 2016 (over EUR 37 million).

Similar trends can be observed in the investment per capita for the acquisition of residential property in the major cities of the country. In 2017, the residents of Vilnius spent the largest amount on the purchase of apartments and houses – EUR 1,626 per capita on average or 1% less than in 2016. The second highest level of housing expenditure per capita was recorded in Klaipėda – EUR 1,049 or 9% more than in 2016. Although Kaunas comes third according to per capita expenditure for the purchase of housing in 2017, the largest positive change was recorded here among the major cities – an average of EUR 809 per capita or a massive 27% increase compared to 2016. The average figure in Šiauliai was EUR 546 (8% more than in 2016) and in Panevėžys – EUR 415 (25% more than in 2016).

Despite a slight increase in mortgage rates in Lithuania, the overall favourable situation in the loan market further stimulated the Lithuanian housing market in 2017. According to the Bank of Lithuania, the average interest rate on new housing loans in 2017 was 2.01% (in 2016 – 1.95% and in 2015 – 1.88%). At the same time the mortgage lending volume and the total housing loan portfolio in Lithuania reached new heights. According to the Bank of Lithuania, in 2017 the remaining loan balance in Lithuania increased by 9.1% to EUR 7.0 billion reaching a historical peak. In 2017, new loans in the amount of EUR 1,178 million were issued in Lithuania and this is almost 12% more than in 2016.

According to the State Enterprise Centre of Registers, the same number of purchase and sale transactions for apartments were concluded in Lithuania in 2017 as in 2016 (33,179 in 2016 and 33,176 in 2017), and 7% more purchase and sale transactions for houses than in 2016 (9,845 in 2016 and 10,529 in 2017). Looking from the historic perspective, the year 2017 was one of the most active in Lithuania and only in 2005 and 2007 the number of residential property transactions was higher. However, trends differ between major cities. In Vilnius, Šiauliai and Klaipėda a decrease in the number of housing transactions (apartments and houses) was recorded compared to 2016: by 6% in Vilnius and Šiauliai and by 2% in Klaipėda. In the meantime, an increase of 5% was recorded in Panevėžys and 4% – in Kaunas. In terms of the relative scope of the transactions per 1,000 citizens, Klaipėda took over the lead from Vilnius in 2017 with the sale of 21.6 apartments/houses per 1,000 citizens, 20.3 – in Vilnius, 18.3 – in Kaunas, 18.0 – in Šiauliai, and 15.3 – in Panevėžys.

Positive economic development in the country encouraged further increase in the prices of the residential property in 2017, yet the relative changes in major cities were somewhat more modest than in 2016. Of all major cities, a faster increase than in 2016 was only recorded in Kaunas. According to data from Ober-Haus, apartment prices in Kaunas increased by an average of 4.8% in 2017 – the price for relatively old apartments increased by an average of 3.0% and for newly constructed apartments – by 8.8%. In Vilnius, Panevėžys, Šiauliai and Klaipėda an increase in the prices of apartments of 3.6%, 3.1%, 2.7% and 2.4% respectively was recorded. The fastest (4% on average) annual growth in the prices of private houses in 2017 was recorded in Vilnius and its suburbs. An increase by an average of 3% in the sale prices of houses was recorded in the regions of Klaipėda, Šiauliai and Panevėžys and an increase by an average of 1% was recorded in Kaunas and its suburbs.

Despite the rapid increase in the supply of apartments for renting in Vilnius over the past years and therefore forecasts regarding a decrease in rents, a symbolic 1% increase in rents was recorded in Vilnius in 2017. The rental market of the capital city remains active and the new supply was substantially absorbed at the same rent levels as in 2016. In the meantime, lower availability of apartments for renting in Kaunas and Klaipėda (especially newly constructed apartments) caused a slightly faster increase in rents in 2017. Rents in Kaunas increased by an average of 4% and in Klaipėda – by 7%. In 2017, the average rent of a 1-3 room apartment in Vilnius was 384 EUR/month, in Kaunas – 295 EUR/month, in Klaipėda – 291 EUR/month, in Šiauliai – 163 EUR/month and in Panevėžys – 137 EUR/month.

The year 2017 saw further growth in investment in construction of new residential buildings in Lithuania. According to Statistics Lithuania, construction works (new construction, reconstruction, repair, restoration, etc.) totalling almost EUR 456 million were performed in the residential property market in 2017 (almost 18% of all construction works performed in the country) or 4.5% less than in 2016 (prices of 2016). However, almost 7% growth in the volume of new construction works was recorded in Lithuania last year.

Experienced developers and higher-class apartment projects prevail

According to data from Ober-Haus, 4,144 apartments in apartment buildings were built in Vilnius in 2017 or 12% more than in 2016. A total of 48 different projects of apartment buildings or their stages were completed in the capital city in 2017. The number of new apartments was the largest since 2008 when 5,471 apartments were built in Vilnius. Projects completed in 2017 were very diverse (in terms of quantity, geography and quality), yet developers tended to invest in the construction of higher class and more expensive apartments. The share of such apartments (the price of the apartments without final fit-out is in excess of 2,000 EUR/sqm) increased from 13% to 18% in the overall annual supply in 2017. These are the projects which offer apartments in the most expensive areas of the city of Vilnius – the centre, the Old Town and other prestigious areas. The share of the medium class apartments (the price of the apartments without final fit-out is between 1,500 EUR/sqm and 1,900 EUR/sqm) in 2017 increased from 48% to 52%. In the meantime, the share of economy class apartments (the price of the apartments without final fit-out is up to 1,500 EUR/m2) decreased from 39% to 30%.

In 2017, experienced developers dominated in the new apartment construction market in Vilnius and the portion of the companies not known in the market (newcomers) decreased compared to 2016. In response to the favourable situation in the market, experienced developers increased their investment portfolio in the residential property market focusing on large-scale projects, while the newcomers developed small projects. Experienced developers, each of which has completed at least four different residential projects, constructed 66% of all apartments in the capital city (in 2016, this figure was 58%). Less experienced developers, each of which has completed 2–3 projects, constructed 24% of all apartments (the figure for 2016 was 21%). The share of apartments constructed by new companies, which do not have any housing development history (i.e. have implemented not more than one project or are only beginning their operations), decreased in 2017 from 21% to 10%. The year 2018 in the apartment market in Vilnius looks promising – construction of at least 4,500 new apartments is scheduled.

More active development of detached and semi-detached houses, which started in 2015–2016, is bearing fruit. In 2017, developers built around 490 new houses in Vilnius and its suburbs or 54% more than in 2016 and twice as many as in 2015. At the same time it is the highest annual supply indicator over the past 15 years (only in 2007, a similar number of houses was supplied to the market). Construction of even a larger number of detached and semi-detached houses is planned in Vilnius and its suburbs in 2018, which could reach up to 550 units. Sales of new houses inspire optimism of developers – at the end of 2017, 85% of the completed houses were sold and reserved.

A rapid increase in supply of newly constructed apartments was recorded in Kaunas in 2017. According to data from Ober-Haus, a total of 547 apartments were built in Kaunas in 2017, which is a 76% increase compared to 2015. The year 2018 promises to be even more productive – construction of 700-800 new apartments in apartment buildings in Kaunas is planned. Six apartment building projects or project stages were implemented in Klaipėda in 2017, which offered 186 apartments (8% less compared to 2016). In the period between 2010 and 2017, on average 200 new apartments in apartment buildings were constructed in Klaipėda each year, but developers did not engage in any further active development projects. However, in 2018 more active development is planned, as a result of which 300–350 new apartments should be offered to the market.

Last year the number of unsold new apartments increased in Vilnius only

The overall decrease in the activity of the new apartment market in major cities in 2017 was due to lower sales volumes in the country’s capital. On the contrary, sales volumes in other cities of the country increased. According to data from Ober-Haus, a total of 4,957 new apartments were purchased or reserved directly from the builders in completed apartment buildings and apartment buildings in progress in Vilnius, Kaunas and Klaipėda in 2017. This was a decrease of almost 7% compared to 2016. In 2017, 3,851 new apartments were sold/reserved in Vilnius, a 12% decrease compared to 2016. This should not come as a surprise, because the sales indicators for new apartments achieved in Vilnius in 2016 were the highest in the past eight years and would be hard to replicate. In 2017, 723 new apartments (a 25% increase compared to 2016) were realised in Kaunas and 383 apartments (a 1% increase compared to 2016) in Klaipėda.

Large scale construction of new apartments in the country’s capital in 2017 determined an increase in the number of vacant apartments in completed apartment buildings while, on the contrary, the figures for Kaunas and Klaipėda decreased. By the end of 2017, the total number of unsold apartments in completed apartment buildings in the three cities was 1,888, which was an increase of 9% compared to 2016. By the end of 2017, 1,359 apartments were offered for sale in apartment buildings in Vilnius built in 2007–2017 (there were 1,013 vacant apartments by the end of 2016); this figure was 151 for Kaunas (239 vacant apartments by the end of 2016) and 378 for Klaipėda (485 vacant apartments by the end of 2016). Until there is any slowdown in the construction of new apartments in the country’s capital, the number of unsold apartments will remain stable or will increase slightly. The largest number of unsold apartments in newly completed apartment buildings was recorded at the end of 2015 and totalled over 1,400. High sales volumes reduced the figure to nearly 900 vacant apartments at the beginning of 2017. The situation in Kaunas and Klaipėda is the opposite – increasing demand for new housing and moderate construction volumes decreased the number of vacant apartments in the course of 2017.

People’s financial capacity for buying housing continues to grow

The ratio between the price of apartments and the level of wages in major cities of the country in 2017 continued to improve for the benefit of buyers. According to Statistics Lithuania, the average net wages in Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys in 2017 increased by 5.6–9.6% on average as compared to 2016. According to data from Ober-Haus, the average price of apartments in these cities over the same period increased by 2.7–5.2% (average prices of 2017 compared to average prices of 2016). So statistically residents of these cities were able to buy more residential property in 2017.

According to data from Ober-Haus, a resident of Vilnius was able to purchase 6.2 sqm in a medium class apartment for the average net annual wage (5.9 sqm in 2016); a resident of Kaunas – 7.9 sqm (7.6 sqm in 2016), a resident of Klaipėda – 8.0 sqm (7.8 sqm in 2016), a resident of Šiauliai – 11.7 sqm (11.3 sqm in 2016) and a resident of Panevėžys – 13.3 sqm (12.7 sqm in 2016).

,Despite the improving statistical ratio between the price of apartments and the level of wages, each case of home purchase may be different. For example, some buyers due to their growing personal needs opt for a more expensive home instead of an affordable home which would be easier to pay for. It is only natural that when borrowing for a more expensive home, the financial burden will be higher, therefore these buyers may not often feel the improving statistical ratio between the price of apartments and the level of wages,’ Mr Reginis said.

Latest news

Ober-Haus Celebrates 25 Years: How Has the Property Market Changed in a Quarter of a Century?

In 1998, the Lithuanian real estate market was characterised by a lack of housing, poor credit conditions and an underdeveloped commercial real estate sector. Over the last 25 years, the number of apartments for sale has increased more than 10-fold, housing market activity has almost quadrupled, lending rates have fallen from double to single digits, and modern office buildings and shopping malls are now numbering in the hundreds – that’s the picture according to the Ober-Haus Real Estate Market Review 1998–2023, conducted to celebrate the company’s 25th anniversary. The Year 2000 Marked the Beginning of the Creation of the Lithuanian Real Estate Market The years 1998–2000 can be considered as the period when the real estate sector in Lithuania began to evolve. Due to the absence of credit services, the Lithuanian population was mostly only able to purchase a home using their own funds, and commercial construction with the intention to sell or lease was in its infancy. And so, 25 years ago, investors were developing single apartment blocks, business/office assets and shopping centres, where any new development for sale or rent was regarded as a significant event in the real estate market. The Russian economic crisis, which began in…

Buyers Show No Interest in Overpriced Housing

The Ober-Haus Apartment Price Index for Lithuania (OHBI), which captures changes in apartment prices in the five largest Lithuanian cities (Vilnius, Kaunas, Klaipėda, Šiauliai and Panevėžys), remained unchanged in September 2023 (August 2023 figures had shown 0.4% growth). The overall level of apartment prices in Lithuania’s major cities grew by 2.6% over the last 12 months (an annual growth of 4.9% in August 2023). In September 2023, Klaipėda, Šiauliai and Panevėžys recorded 0.2%, 0.3% and 0.4% growth respectively, and the average price per square metre rose to EUR 1,613 (+3 €/m²), EUR 1,103 (+3 €/m²) and EUR 1,078 (+4 €/m²). Meanwhile, in Vilnius and Kaunas, the average price per square metre decreased by 0.1% month-on-month to 2.568 Eur (-3 €/m²) and 1.724 Eur (-2 €/m²) respectively. Over the year (September 2023 as compared to September 2022), apartment prices grew in all major cities of the country: in Vilnius – by 2.6%, in Kaunas – by 3.2%, in Klaipėda – by 1.6%, in Šiauliai – by 3.7%, and in Panevėžys – by 2.5%. The stagnation period in the Lithuanian housing market continues. Although the market activity indicators do not show any signs of improvement, the majority of home sellers have not…

Office sublease: thousands of invisible square metres

In the office segment, the phenomenon of sublease – the transfer of part of a company’s leased premises to a third party – became popular during the pandemic and has remained since. The market of subleased property is usually not included in the official statistics published by real estate agencies. According to OBER-HAUS, current tenants of Class A and Class B+ business centres in Vilnius alone could be offering several thousand or even tens of thousands of square metres of space for sublease. Sublease is usually simply understood as renting space not directly from the owner or manager of a business centre, but from an existing tenant established and operating in the business centre. The principle of sublease itself existed long before the pandemic, but has only become more popular in recent years as businesses switched to remote or hybrid work, consequently, the amount of space required for their operations has decreased. OBER-HAUS estimates that since the beginning of the pandemic, the average office space in Vilnius has decreased by about 30%. In other words, companies entering into new contracts today are renting office space by almost a third smaller than a few years ago. However, office lease contracts are…